Skip to main content

Skip to main content

What is PSLF?

Public Service Loan Forgiveness (PSLF) is a federal program that forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments (approximately 10 years) under a qualifying repayment plan while working full-time for an eligible public employer.

Upcoming Webinars

Upcoming Webinars

Public Service Loan Forgiveness (PSLF): 2026 Updates

Wednesday, September 16, 12 p.m.

Are you pursuing Public Service Loan Forgiveness (PSLF)? Confused about all the new changes to student loans? Join us to learn how federal student loan changes affect borrowers pursuing PSLF.

In this webinar, we will cover:

- PSLF program overview

- PSLF Buyback program

- July 1 changes affecting PSLF

- Parent PLUS Loans and PSLF

- Recent PSLF court decisions

Presenters:

Amber Hay (she/her), PSLF Advocate

Terri Parker (she/her), PSLF Policy & Performance Analyst

Jessica Manfredi (she/her), Student Loan Advocate

Note: While we will touch on how SAVE interacts with PSLF borrowers, please check out our recent webinar for guidance on exiting the SAVE forbearance.

Past Webinars

Past Webinars

Navigating Federal Student Loan Repayment: Life after SAVE & Avoiding Default - 6/30/2026

Are you confused about what to do now that the SAVE forbearance is coming to an end? Watch our webinar to learn about the federal student loan repayment options available to borrowers. This webinar features Student Loan Advocates and Ombudspersons from California, the District of Columbia, Illinois, Maryland, Massachusetts, Nevada, North Carolina, Virginia, and Washington.

We discuss what to expect as the SAVE forbearance ends, review repayment and forgiveness options, and outline steps borrowers can take to avoid delinquency and default. Participants also learned about income-driven repayment plans vs. fixed repayment plans, temporary relief options like forbearance and deferment, and important timelines and deadlines. The session concluded with guidance on available tools and resources to help borrowers navigate repayment moving forward.

You may also access the presentation slides (PDF, 656.14 KB) and transcript (PDF, 139.1 KB).

Navigating the Future of Student Loans: Insights from State Ombudsmen and Advocates webinar – 3/18/2026

This webinar features state student loan Ombudsmen and Advocates from California, Connecticut, the District of Columbia, Illinois, Maine, Minnesota, Nevada, Oregon, and Washington. We discuss the latest updates on federal student loans, vital borrower resources, and how these offices can assist you. As significant changes are on the horizon for 2026, this webinar helps you understand how these updates may affect your options moving forward.

We cover essential topics, including borrower rights, repayment plans, new borrowing limits, Public Service Loan Forgiveness (PSLF), default management, and more. This session is open to all students—both new and existing borrowers—as well as parent borrowers. Don’t miss this opportunity to gain crucial insights and support in navigating the evolving student loan landscape!

You may also access the presentation slides (PDF, 575.51 KB) and transcript (PDF, 172.56 KB).

Public Service Loan Forgiveness (PSLF): Overview and Updates - 11/19/2025

Have you heard about the Public Service Loan Forgiveness (PSLF) program, but are not sure if you qualify? Do you want to learn more about how other student loan changes & updates impact PSLF? In this webinar from November 19, 2025, you will get an overview of the PSLF program, including:

- Steps to apply and stay eligible for PSLF.

- Using Studentaid.gov to track your PSLF progress.

- How the PSLF Buyback program works.

- The impacts of recent federal legislation and rulemaking on PSLF.

You may also access the presentation slides (PDF) and transcript (PDF, 171.24 KB).

Understanding Changes to Federal Student Loans - 9/17/2025

Do you want to learn what is happening in the world of student loans right now? Do you have questions about the SAVE forbearance and how it impacts your eligibility for forgiveness? Are you confused about how the “One Big, Beautiful Bill Act” will affect your student loans? In this webinar, you will get an overview of updates to federal student loans, including:

- SAVE forbearance and options to remain eligible for Income-Driven Repayment (IDR) or Public Service Loan Forgiveness (PSLF).

- How the “One Big, Beautiful Bill Act” is drastically changing federal student loan borrowing and repayment options.

- Status of the Public Service Loan Forgiveness (PSLF) program.

- Changes to other Federal Student Aid programs, including Total and Permanent Disability Discharge (TPD), and the Joint Consolidation Separation process.

You may also access the presentation slides (PDF, 6.34 MB) and transcript (PDF, 521.31 KB).

Stay Informed

Stay Informed

Sign up for email updates from the Office of Student Loan Advocacy to receive info about future webinars and other important student loan announcements and news.

Contact Us

Contact Us

To ask questions about your loans (including PSLF and other types of forgiveness) or file a complaint, use the Washington State Student Complaint Portal.

A member of our Student Loan Advocacy team will be happy to help you.

Ask us about:

- Income-driven repayment (IDR).

- Public Service Loan Forgiveness (PSLF).

- Delinquency and default.

- Deferment and forbearance.

- Total and Permanent Disability (TPD) discharge.

- Closed school discharge.

- Consolidation.

- Other student loan questions.

Timeline: PSLF outcomes for Washington borrowers

Use the tabs below to learn about the program rules, special opportunities to earn PSLF qualifying payments, and resources to navigate the PSLF process.

Normal PSLF Rules

Normal PSLF Rules

Borrowers who work an average of 30+ hours per week at a public service job could be eligible for debt forgiveness if they meet the requirements:

- Be employed by a U.S. federal, state, local, or tribal government or qualifying not-for-profit organization (federal service includes U.S. military service);

- Have Direct Loans (or consolidate other federal student loans into a Direct Loan);

- Repay your loans under an income-driven repayment plan or a 10-year Standard Repayment Plan; and

- Make a total of 120 qualifying monthly payments (about 10 years).

Learn more on Federal Student Aid’s Public Service Loan Forgiveness (PSLF) page.

Learn how to manage your Public Service Loan Forgiveness progress on StudentAid.gov.

IDR Payment Count Adjustment – 2024

IDR Payment Count Adjustment – 2024

In the past, there were a variety of reasons why some months may not have been credited toward Income-Driven Repayment (IDR) loan forgiveness and Public Service Loan Forgiveness (PSLF)—for example, months when you were in a payment plan that wasn’t eligible.

ED conducted an adjustment of IDR-qualifying payments for all William D. Ford Federal Direct Loan (Direct Loan) Program and federally owened Federal Family Education Loan (FFEL) Program loans.

The payment count adjustment counted time toward IDR forgiveness, including:

- Any months in a repayment status, regardless of the payments made, loan type, or repayment plan;

- Twelve or more months of consecutive forbearance or 36 or more total months of forbearance prior to July 1, 2024;

- Any months spent in economic hardship or military deferments in 2013 or later;

- Any months spent in any deferment (with the exception of in-school deferment) prior to 2013; and

- Any time in repayment (or deferment or forbearance, if applicable) on earlier loans before consolidation of those loans into a consolidation loan.

Please note, repayment status does not include periods of in-school deferment, bankruptcy, or default.

Borrowers who submitted a consolidation application on or before June 30, 2024, and whose consolidation loan was disbursed before Oct. 1, 2024, had the payment count adjustment applied to their new Direct Consolidation Loan.

Effects on Public Service Loan Forgiveness (PSLF) Applicants:

- Borrowers with at least one approved PSLF form began to see their PSLF counts adjusted in Fall 2023.

- Borrowers who consolidate will have their PSLF counts temporarily reset to zero, and these counts will begin adjusting in Fall 2023.

- IDR and PSLF counts were adjusted for all federally held FFELP and Direct Loans by December 2024.

- All periods credited toward IDR will also be credited toward PSLF for eligible loans and periods where the borrower certifies public service employment.

- If you’ve applied or will apply for PSLF and certify your employment, you may see the benefits of this adjustment to your qualifying payment count.

- These changes were applied automatically to all PSLF-eligible Direct Loans, including consolidated and unconsolidated Parent PLUS loans.

- If you believe you might benefit, use the PSLF Help Tool to certify periods of employment and track your progress toward forgiveness.

- Borrowers with commercially or federally held FFEL loans needed to apply to consolidate those loans into Direct Consolidation Loans by June 30, 2024, to get PSLF credit under the payment count adjustment.

Learn more and read the Q&A on the Payment Count Adjustment page.

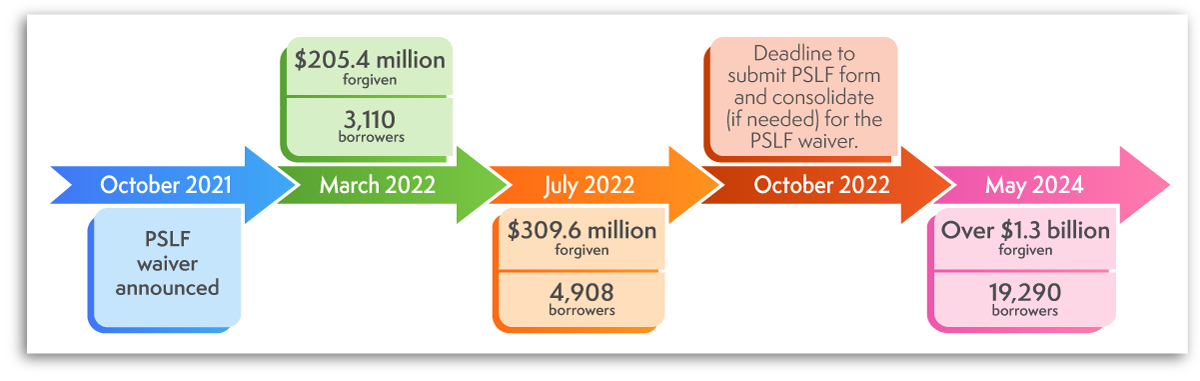

PSLF Waiver – 2022

PSLF Waiver – 2022

The Public Service Loan Forgiveness (PSLF) limited time waiver period ended on October 31, 2022. If you have any questions about the waiver, please submit a request.

On October 6, 2021, the U.S. Department of Education (ED) announced a new limited waiver opportunity for the PSLF program. For a limited time, borrowers could receive credit for past payments that had not previously qualified for PSLF.

Under this limited waiver opportunity, any prior payment made on a Federal Family Education Loan (FFEL), Federal Perkins Loan, or other non-direct federal student loan will count as a qualifying payment, regardless of repayment plan, or whether the payment was made in full or on time. All you needed was a qualifying employment and a Direct Loan. The waiver only applied to loans taken out by students, not parents.

In order to secure a review under the limited waiver opportunity, you may have needed to act by October 31, 2022. Please visit ED’s PSLF limited waiver opportunity webpage to find out what steps you needed to take, if any. For example:

- If borrowers had a loan type that does not normally qualify for PSLF, including a Federal Family Education Loan (FFEL) or Federal Perkins Loan, they needed to consolidate that loan into the Direct Loan program by October 31, 2022.

- If borrowers had not submitted a certification for all periods of qualifying employment, they needed to submit a PSLF form via the PSLF Help Tool for any uncertified employment period by October 31, 2022.

Direct Loan borrowers who had previously submitted certifications from their employers will receive automatic updates of their qualifying payment counts for the certified employment periods. However, it could take several months for these updates to appear.

Please note that Parent PLUS loans were not eligible for the limited waiver opportunity unless they were consolidated with loans from the parent’s own education.

PSLF and Direct Parent Plus Loans

PSLF and Direct Parent Plus Loans

Parent PLUS Loans are federal loans taken out by parents to help pay for their children’s education. Many Direct Parent PLUS borrowers ask us “Am I eligible for PSLF?”

The answer depends on when your Direct Parent PLUS Loans are issued.

Parent PLUS Loans Borrowed before July 1, 2026

- Borrowers with unconsolidated Parent PLUS loans may need to act to keep access to Income-Driven Repayment (IDR) plans and PSLF. Parent PLUS borrowers will need to have successfully completed consolidation of their Parent PLUS Loan(s) by June 30, 2026, and enroll into Income-Driven Repayment (IDR) by July 1, 2028. This means the new loan must be issued by June 30, 2026.

- For more information, including specific steps to take, check out the Parent PLUS Checklist & Resource Guide (EDCAPNY.org) (PDF).

- Borrowers with unconsolidated Parent PLUS Loans who choose not to consolidate, may enroll in the 10-year Standard Plan to make progress towards PSLF. This plan may lead to no amounts forgiven at the end of the 120 qualifying payments for PSLF. In order to have a balance left to forgive under the 10-year Standard Plan, you will need to have at least some periods under eligible forbearance and deferment status (such as the COVID-19 administrative forbearance) while working at a qualifying public employer.

- Borrowers who have already consolidated their Parent PLUS Loans, with a single or double consolidation, will retain access to Income-Contingent Repayment (ICR) until July 1, 2028.

- After making at least one payment on the ICR plan, these borrowers can now access the Income-Based Repayment (IBR) plan by filling out a new IDR application. IBR monthly payments may be less than payments under ICR.

Parent PLUS Loans Borrowed after July 1, 2026

- New Parent PLUS loan borrowers after July 1, 2026, will have access to one repayment plan, the new Tiered Standard Plan. Payments under this plan do not qualify for PSLF.

- These borrowers will be unable to access a PSLF qualifying repayment plan and will be unable to pursue PSLF.

Risks of borrowing any federal loans on or after July 1, 2026, for parent borrowers:

- If you take out or consolidate any federal loans on or after July 1, 2026, your Parent PLUS Loans, Consolidation Loans that included any Parent PLUS Loans, and “double consolidated” Parent PLUS loans will be restricted to the new Tiered Standard plan.

- In most cases, this will block you from pursuing PSLF for these loan types as you will not have access to a PSLF-qualifying repayment plan. This will also block you from pursuing IDR forgiveness.

- In short, taking out any new loans after July 1, 2026 will stop you from accessing PSLF for your existing loans that include Parent PLUS Loans.

PSLF Buyback

Public Service Loan Forgiveness (PSLF) Buyback

PSLF Buyback allows borrowers to buy back certain months in normally ineligible forbearance or deferment statuses to make them qualifying payments for PSLF. Please review the Federal Student Aid’s PSLF Buyback website for information on how PSLF Buyback works.

Please be advised that our office cannot speed up the processing of your PSLF Buyback request/application.

Unfortunately, there is a large backlog of unprocessed PSLF Buyback request. It could take 1-2 years for requests to be processed, and duplicate requests will not result in faster processing.

PSLF Buyback and SAVE Forbearance

If you are still on the SAVE forbearance waiting for your PSLF Buyback application to process, you need to decide what action to take before the SAVE forbearance ends.

Action Options:

- Apply for another PSLF qualifying repayment plan.

- Pros: Continue to make payments towards forgiveness. May lead to forgiveness faster. These payments would also reduce the number of months you need to Buyback.

- Cons: Monthly payments may be higher than what buying back those older months would be.

- Contact your student loan servicer and request to be placed on a discretionary forbearance while you wait for Buyback processing.

- Pros: No monthly payments would be required – giving time to save up for the Buyback amount.

- Cons: Interest accrues and forbearance doesn’t count towards PSLF. There is a limit on amount of time you can spend in a discretionary forbearance and Buyback processing time is still unknown. Your Buyback application could be denied, and you may need to resume repayment at that point to reach forgiveness.

Note: PSLF Buyback amounts for the SAVE forbearance time will NOT be calculated using the SAVE plan formula. This means that payments for those months will likely be higher than you may have expected when you applied for Buyback.

How do I apply for PSLF?

Use the tabs below to learn more about the PSLF process and the steps you need to take to receive forgiveness under the program.

Quick PSLF Overview

Quick PSLF Overview

For a quick, easy to understand explanation of the program, please check out the How to Get your Student Loans Forgiven (No, Really) (PDF) handout.

Steps to Apply for PSLF

Steps to Apply for PSLF

Do you want to apply for PSLF but don’t know where to start? Check out the Steps to Apply for PSLF (PDF) for step-by-step guidance on how to apply and remain eligible for PSLF.

PSLF Frequently Asked Questions

PSLF Frequently Asked Questions

Do you have general questions about the PSLF program? Check out the Public Service Loan Forgiveness (PSLF) FAQs (PDF) to find answers to the most frequently asked questions about the program.

Information for Employers

Information for Washington State Agencies and Public Institutions of Higher Education

In March 2022, in response to the student loan debt crisis facing the country, the state Legislature passed legislation to raise awareness and remove barriers for public service employees to access the PSLF program with specific requirements for Washington state agencies and public institutions of higher education (ESSB 5847, codified as RCW 28B.77.009, RCW 43.41.425, RCW 41.04.045, and RCW 41.04.055).

Office of Financial Management (OFM) created a webpage and HR portal to provide guidance to Washington state agencies and public institutions of higher education on how to comply to the new regulations.

Information for Local Municipalities and Nonprofit Organizations

Local government agencies, like cities, counties, tribal government, and nonprofits are a significant part of the public sector workforce. You as an employer play an essential role in helping borrowers receive Public Service Loan Forgiveness (PSLF). Do you want to help your employees benefit from PSLF, but are not sure how?

As part of our efforts to make the certification process easier for local government agencies and qualifying nonprofit organizations located in Washington state, we have created in partnership with the Office of Financial Management (OFM), the following notice templates you can use to support your employees on their path toward loan forgiveness:

- PSLF Notice for New Employees. We recommend sharing this letter (Eligibility Letter for Web (Word Doc) or Eligibility Letter for Print (Word Doc) version) with employees upon hiring, during the onboarding process to introduce the PSLF program and process.

- PSLF Annual Notice. We recommend sharing this letter (PSLF Annual Notice - Web (Word Doc) or PSLF Annual Notice - Print (Word Doc) version) with employees on an annual basis and any time PSLF regulations change (see below) to continue raising awareness of the program and the resources available.

- PSLF Notice for Separated Employees. We recommend sharing this letter (PSLF Notice - Web (Word Doc) or PSLF Notice - Print (Word Doc) version) with employees during the separation process, so they know which steps to take to receive and potentially continue receiving PSLF credit.

PSLF program regulations may change from time to time. We will periodically update the letters to reflect the most up-to-date PSLF rules. If you would like to receive updates when these materials are updated, please join our mailing list.

We’re here to assist PSLF employers! If you have any questions about the PSLF process as an employer, please send your question(s) to PSLF@ofm.wa.gov.

Additional Resources:

- Check out detailed guidance on which nonprofit organizations qualify for PSLF.

- Check out Federal Student Aid’s employer tips on tacking the PSLF form

- Check out Federal Student Aid’s guidance on the employer’s role in PSLF

- Check out step-by-step instructions on how to use the PSLF Help Tool DocuSign (PDF) feature as an employer

- Find out the acceptable signature methods on manual PSLF Forms.

Public Service Loan Forgiveness (PSLF): Guidance for Local Government Employers (6/10/25)

As of December 2024, 23,900 public service employees in Washington have received over $1.66 billion in federal student loan forgiveness through the PSLF program.

47 percent of recently surveyed employees said that the promise of earning loan forgiveness through PSLF affected their decision to begin working in public service, while 65 percent said that PSLF influenced their decision to stay for at least 10 years.

In this webinar, learn how counties, municipalities, tribal governments, and other local government employers can use PSLF as a no-cost tool to recruit and retain employees. We’ll cover:

- An overview of the PSLF program

- PSLF best practices for employers

- Resources for employers

You may also access the presentation slides (PDF) and transcript (PDF).

PSLF Employer Resources & Tips for the Nonprofit Association of WA (9/19/24)

Public Service Loan Forgiveness (PSLF) is a federal program that forgives the remaining balance on Direct Loans for public service employees. Between March 2022 and May 2024, 19,220 public service employees in Washington state have received a total of $1.3 billion dollars in federal student loan forgiveness through the PSLF program.

As a nonprofit employer, learn how you can utilize PSLF as a no-cost tool to recruit and retain your employees. In this webinar, we cover:

- An overview of the PSLF program

- How public service employers can help employees access PSLF

- PSLF resources for employers and employees

- How the Office of the Student Loan Advocate can support employees on their path to forgiveness.

You may also access the presentation slides (PDF, 3.89 MB) and transcript (PDF, 193.71 KB).

Information for Washington State Employees

Washington State Directory for PSLF Contacts

If you are completing your PSLF form and need to find your current or former agency's Employer Identification Number (EIN) or HR contact information, refer to Washington state agency directory of PSLF contacts.

The directory includes Employer Identification Numbers (EINs) and HR email addresses for each agency, which are required for employees to complete the PSLF form on the PSLF Help Tool.

Part-time Academic Employees Full-time Calculation

Are you a part-time academic employee (commonly known as “adjunct faculty”) at a public institution of higher education? Did you know that according to RCW 41.04.055, your human resources department at public institutions of higher education must multiply part-time faculty’s in-class teaching hours by 3.35 to calculate your hours worked for the PSLF form? This is to account for duties performed in support of, or in addition to, contractually assigned in-class teaching hours.

Your human resources department may apply this calculation retroactively to figure out whether the U.S. Department of Education considers a part-time academic employee “full time” for the PSLF form. Please note that this calculation does not supersede any calculation or adjustment set up in the collective bargaining agreements or higher education institution policies.

SAVE Litigation Impacting PSLF

SAVE Litigation Impacting PSLF

Public Service Loan Forgiveness (PSLF) requires borrowers to be on an income-driven repayment (IDR) plan (or the 10-year standard repayment plan). Since the return to repayment in 2023, many student loan borrowers seeking PSLF opted into the SAVE IDR plan that offered more generous benefits.

- The U.S. Court of Appeals for the 8th Circuit has issued a ruling that the Saving on a Valuable Education (SAVE) Plan is not a legally authorized repayment plan and will be discontinued. Beginning July 1, federal loan servicers will send notices to borrowers currently enrolled in the SAVE Plan with instructions on selecting a new, eligible repayment option.

- What this means for you:

- You will receive a notice from your servicer about your specific 90-day deadline to select a different repayment plan.

- You will have 90 days from the date of your notice to choose a new repayment plan.

- If you do not select a plan within that timeframe, you will be automatically enrolled in the Standard Repayment Plan.

- Our office strongly recommends SAVE borrowers start exploring their other repayment options as soon as possible. Check out this guide to help you understand your options: Transitioning From the SAVE Repayment Plan (EDCAPNY.org).

- Stay informed: Get updates and more information on the U.S. Dept. of Education's website.

- Time spent in the SAVE Forbearance is eligible for PSLF Buyback. Borrowers with 120 months of eligible PSLF employment can buy back (make payments to cover) past months that were not originally counted as qualifying payments due to the SAVE Forbearance.However, the SAVE formula cannot be used to calculate Buyback amounts for time spent in the SAVE forbearance. This means that your PSLF Buyback amount for months in the SAVE forbearance may be significantly higher than you may have predicted.

Stay informed: Get updates and more information on the effects of the SAVE litigation on the U.S. Dept. of Education's website.

About the student loan advocate

The student loan advocate has independent statutory authority to analyze and monitor laws and policies that impact student loan borrowers at the federal, state, and local level, and to make recommendations. The student loan advocate also works directly with loan borrowers to address complaints and help them navigate issues and identify resources.